What is Blockchain?

Blockchain. It’s a term that’s been on the tip of everyone’s tongue following recent, exciting advances in the technology, and growing media attention on the cryptocurrency market. Rightfully so, there is also a healthy mix of skepticism and cautious optimism depending on who you speak with. This year’s Health Datapalooza program aims to address the hype with multiple sessions including a main stage panel titled “AI, Blockchain, Machine Learning, IOT...from Buzzwords to Reality in Healthcare.” We hope this two-part blog will help you understand how blockchain works, considerations for health-related applications, and what the future holds.

At its core, blockchain technology represents a data structure that makes it possible to create a digital ledger of transactions and share it among a distributed network of computers with the potential for increased security, reductions in cost, decreased transaction times, and greater transparency - all while eliminating the need for a trusted third-party or intermediary. Blockchain technology uses cryptography to allow each participant in the network to make additions to the ledger in a secure manner without the need for a central authority, as long as any additions and changes are validated and agreed upon by network participants as adhering to the rules of the specific blockchain protocol.

Blockchain technology, conceptualized by early pioneers such as the pseudonymous programmer(s) Satoshi Nakamoto with the widely known Bitcoin blockchain platform, was crafted in response to problems related to trust and the need for disintermediation in transaction processing. Blockchain’s elimination of central authorities, third-parties, or intermediaries for common transactions result in ‘trustless’ transactions where two parties conduct a transaction (i.e., peer-to-peer) by trusting the rules and cryptography in the underlying blockchain protocol. These features alleviate the common double spend problem (i.e., using the same digital money files such as Bitcoins more than once) with blockchain transactions structured to be irreversible and final within their timestamped universal ledger.

Blockchain technology can also be classified into three categories based upon the entities who control and participate in the specific blockchain platform ecosystem: Private, permissioned, and public.

Private blockchains are controlled by single entities managing all of the nodes and validators (i.e., key members of the organization’s blockchain network which independently check the data being conveyed through the network). Their distributed ledgers provide auditability of transactions within an organization, and the self-contained nature promotes privacy versus public blockchains. However, private blockchains lack true decentralization, leaving them potentially susceptible to the dictates of centralized governance and decision making. Attackers targeting an organization’s validator nodes, can also lead to the risk of blockchain rule changes or ledger modifications which compromises the integrity of the blockchain.

Permissioned, or consortium, blockchains are those in which a group of participants (typically in a formal business agreement) each run a validator node. This promotes greater decentralization than private blockchains depending on the number of participants and validator nodes in the system. However, potential collusion between a majority participants or compromising the majority of validator nodes can result in a compromised blockchain. Permissioned blockchains have shown promise for multiple parties focused on eliminating issues of trust within their network using a transparent ledger supporting inter-party transactions. Permissioned and private blockchains afford greater privacy and transaction throughput with fewer validator and participating nodes, at the cost of security and potentially immutability.

Public blockchains, like the Bitcoin and Ethereum® platforms, allow anyone with a computer and internet connection to participate by downloading the necessary client software to run a node, regardless of whether they choose to actively conduct transactions or act as a validator. Public blockchains offer the greatest degree of decentralization, security, and likelihood of a ledger remaining immutable, at the cost of lower throughput, greater overhead in the form of transaction fees (typically paid to nodes that secure the network and confirm transactions), and lack of substantial privacy controls. These limitations make public blockchains a more difficult proposition for organizations from a data security/anonymity standpoint, though some interesting breakthroughs on are on the horizon in this regard.

As with the internet, which evolved from smaller networks or intranets, it is likely that many participants will initially gravitate towards private or permissioned blockchain technology. As the technology matures and new applications beyond cryptocurrency gain traction, the advantages of public blockchains will help advance their use.

Okay, but HOW does it work?

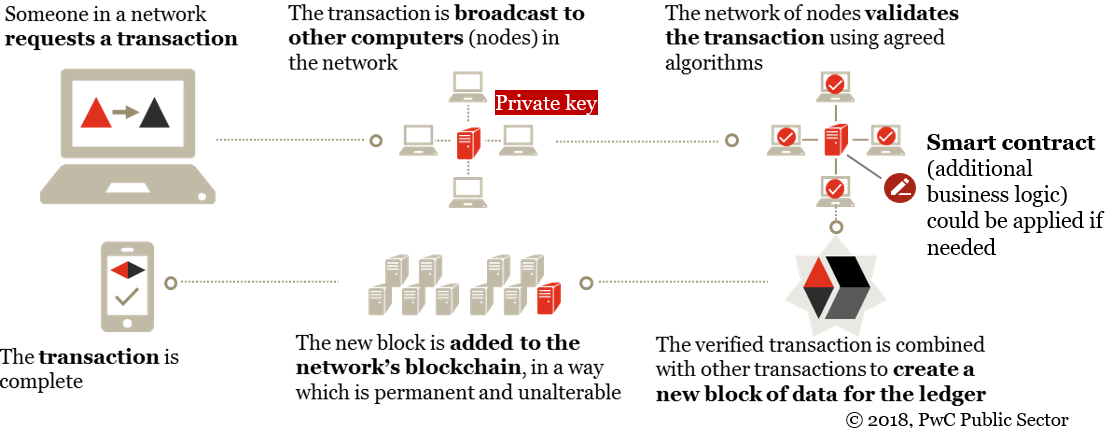

The general concept of blockchain technology is that it represents a distributed, decentralized ledger that is secured cryptographically and, except under rare circumstances, immutable. The following figure outlines the processes occurring on a public blockchain from transaction origination to confirmation.

Blockchain can be perceived as a key for a specific lock on a specific door, rather than a master key for doorway. There are additional nuances with various blockchain protocols and applications in addition to distinctions between public, permissioned, and private blockchains. These differences result in potential trade-offs and should be assessed by any organization considering the application of blockchain to their business.

When should I consider blockchain?

Ultimately, blockchain technology brings a new and potentially game-changing solution to help address traditionally challenging issues of trust and the secure exchange of information in many multi-party transactional processes. In the context of health care, whether it’s health records and registries, claims processing, aid disbursement, or provenance in supply chain or chain of custody, blockchain can help close the trust gap through trustless, mathematically verifiable transactions, the elimination of intermediaries in a decentralized peer-to-peer network, and automation of conditional agreements.

The advent of more advanced blockchain platforms such as Ethereum® and Hyperledger™ (which comprises multiple blockchain technologies) offer the capability to incorporate logic-based, conditional agreements commonly referred to as “smart contracts” which can support the automation of transactions based on coded conditions and logic. This capability greatly expands the potential use cases for blockchain beyond peer-to-peer payments and simple value transactions to more ambitious applications built on an “Internet of Agreement” such as:

- Blockchain enabled crowdfunding;

- Supply chain management and other provenance-based use cases;

- Identity verification, management, and eventually, self-sovereign identity;

- Registries (Birth, Death, Land, Voting, etc.);

- Asset management (tokenizing physical assets on the blockchain);

- Decentralized data storage and dissemination;

- Unique incentive programs for cross-market use; and,

- Many more… it’s likely the best use cases have not even been thought of yet!

These use cases show exciting potential as blockchain technology matures at a rapid pace. Bitcoin, the oldest blockchain, has been around for eight years but has only gained widespread use in the past year. Other blockchain platforms such as Ethereum® and Hyperledger’s suite of solutions face a number of challenges - from scalability and access (most of the public blockchains have not achieved widespread use and scalability), to security and privacy protection, the technology and processes underlying blockchain are rapidly evolving and will take time to mature which makes a strong case for small scale projects and piloting proof of concepts.Whatever its ultimate use, blockchain technology can no longer be ignored by the federal, commercial, and non-profit health care sectors which rely upon the secure exchange of highly sensitive information. Stakeholders in the health care ecosystem are starting to get their feet wet with blockchain. Collaborations abound and an increasing interest in small projects and pilot initiatives to allow organizations test the technology – and their risk tolerance. While prudence is necessary, the significant potential advantages of blockchain technology present an incredible opportunity for early adopters in health care.

Please stay tuned for our second blog post which will further explore specific applications of blockchain and expand on the future potential for this exciting technology in research, clinical, and public health.